Rise in global population and the resulting growth in production, consumption and distribution has a tremendous impact on the earth’s natural systems. These impacts include rising atmospheric and surface water temperatures, as well as long-term changes in weather patterns. Left unchecked, the consequences of our actions can be catastrophic. It is therefore extremely crucial to measure, monitor and mitigate climate risks. Carbon Accounting plays a fundamental role in understanding and assessing climate risks.

To get familiarized with ‘carbon accounting’, it is important to ask the right questions –

What is Carbon Accounting?

Carbon accounting is the process by which organizations quantify or estimate emissions and greenhouse gasses (GHG) released from the creation of a process, product, or service and transform it into the carbon equivalent. Through this process carbon or greenhouse gas inventory is maintained in order to understand the organization’s climate impact and set goals to limit their emissions. Carbon accounting was established under the Kyoto Protocol, a treaty written up and agreed upon in an effort to reduce emissions that can alter the climate. In simple terms, carbon accounting is a method for tracking carbon emissions.

Why is it important?

Carbon accounting is important to organizations for a number of reasons including, potential cost-cutting implications, identification of risks and opportunities, opportunity to showcase environmental leadership and competitive advantage as well as regulatory requirements. It plays an integral part of corporate social responsibility by improving a company’s reputation and building accountability

Who should account their carbon emissions?

Businesses are the frontrunners when it comes to carbon accounting as they have large carbon footprints. They also have the resources to maintain carbon inventories and account for their emissions. Many governments at national and state levels are also estimating their regions’ emissions. Carbon accounting can be conducted at an individual level as well.

How is it carried out?

There are two widely used methods for carbon accounting, the life-cycle assessment methodology (ISO), and the GHG protocol from the World Resources Institute and the Intergovernmental Panel for Climate Change (IPCC). ISO 14064 specifies principles, guidelines and requirements for quantification and reporting of greenhouse gas (GHG) emissions at an organizational or project level. It includes requirements for the design, development, management, reporting and verification of an organization’s GHG inventory. The GHG Protocol is a comprehensive global standardized framework to measure and GHG emissions from private and public sector operations, value chains and mitigation actions

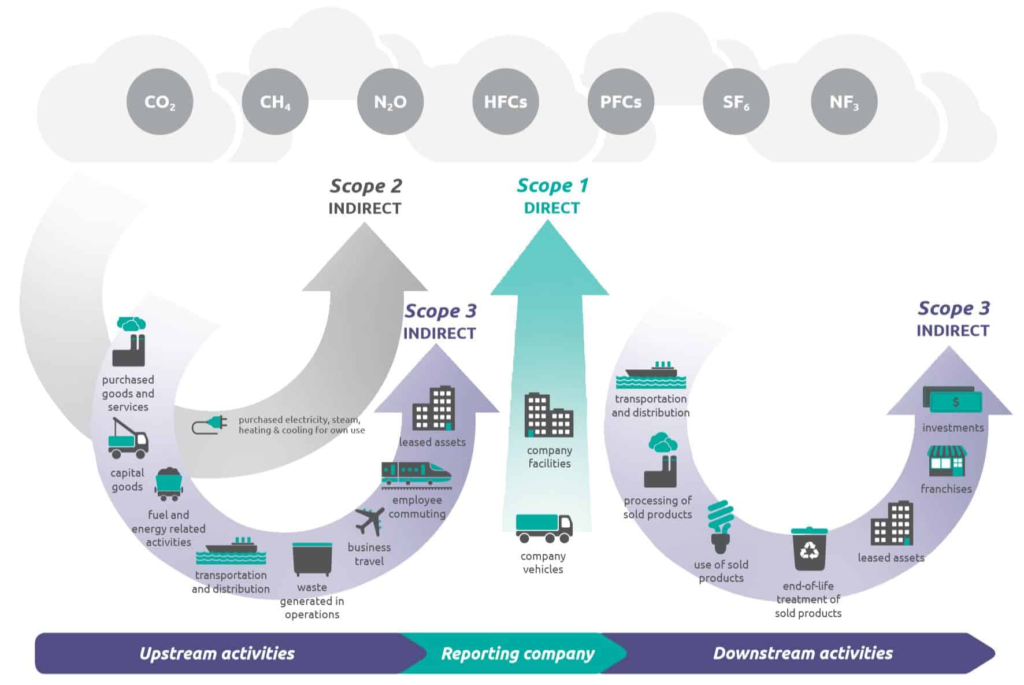

The GHG protocol characterizes emissions as direct (Scope 1) and indirect (Scope 2 & 3) to improve transparency, and provide utility for different types of organizations, climate policies and business goals. Scope 1 accounts for all direct GHG emissions that occur from sources that are owned or controlled by the company, for example, emissions from combustion in owned or controlled boilers, furnaces, vehicles, etc. Scope 2 accounts for GHG emissions from the generation of purchased electricity consumed by a company. These emissions physically occur at the facility where electricity is generated. Scope 3 accounts for all indirect emissions that occur throughout the value chain (upstream and downstream), classified into 15 categories. Emissions that are a consequence of the activities of the company, but occur from sources not owned or controlled by the company. Some examples of scope 3 activities are extraction and production of purchased materials; transportation of purchased fuels; and use of products and services.

Most companies that follow the GHG protocol, start with estimating Scope 1 and Scope 2 emissions as the data required is typically readily available. Scope 3 is an optional category but an essential category as most often we find it is the largest contributor to an organization’s overall emissions. Estimating scope 3 emissions is challenging as the data collection process can be tedious.

What do you do after you estimate your organization’s emissions?

Once organizations measure and estimate their emissions, they will be in a position to set emission reduction targets and accordingly formulate policies and practices to achieve these targets. Organizations usually set carbon reduction targets by establishing a base year, a percentage reduction and aligning with a target year – 2030, 2050, etc. Some even establish ‘net zero’ or ‘carbon neutral’ targets. It is important to disclose targets and the progress towards achieving the targets by working with organizations such as CDP, TCFD, SBTi and others.

Starting the carbon accounting process for an organization can be daunting. But change begins with measuring. A great place to start is to reach out to professionals and experts in the field for consultation on carbon accounting, defining boundaries, identifying priority areas and setting goals.

Get in touch with Sage Sustainability for more on Carbon Accounting.

Sources:

1. What is Carbon Accounting and Why is it Important? (June 2020)

https://www.opensourcedworkplace.com/news/what-is-carbon-accounting-and-why-is-it-important

2. Why Carbon Accounting Matters, Triodos Bank (2019)https://www.triodos.com/articles/2019/why-carbon-accounting-matters

3. India Inc already seeing benefits of carbon accounting, Megha Jain & Aishwarya Nagpal (2019)4. India GHG Program https://indiaghgp.org/explaining-scope-1-2-3

5. GHG Protocol